Blog

Digital Banking Testing: A Guide for Neobanks

Published on

June 29, 2026

Why digital banking testing is a survival function, the five hardest testing challenges neobanks face, and how AI-native testing keeps pace with releases.

In digital banking, the interface is the entire institution. There is no branch to fall back on and no teller to smooth over a glitch, so when a transfer fails silently, a balance loads incorrectly on a tablet, or an onboarding flow breaks on a specific Android browser, the bank has not just lost a transaction. It has lost trust, and in financial services trust is the only product that matters.

This guide sets out why digital banking testing has become a survival function rather than a quality-assurance afterthought, the five hardest challenges it presents, why legacy automation fails at neobank release velocity, and how AI-native testing changes the economics.

The neobanking market is growing at a pace almost no other sector matches. According to Fortune Business Insights, it is projected to grow from around 310 billion dollars in 2026 to over 7.6 trillion dollars by 2034, a compound annual growth rate above 49 percent.

The user picture is more consistent across sources. Neobank users worldwide are expected to surpass 350 million in 2026, and Millennials and Gen Z already make up around 78 percent of the global neobank customer base. These are users who will abandon a banking platform faster than they will close a social media tab, and they are testing the application on hundreds of device, browser, and operating-system combinations it was never explicitly designed for.

That is why digital banking testing is no longer just a quality-assurance function. It is a survival function, and a testing strategy built for monolithic core banking systems with quarterly releases is already obsolete.

Traditional banking software lived behind firewalls, on internal networks, accessed by employees through standardised workstations, which made testing it straightforward, with controlled environments, known configurations, and predictable user behaviour.

Digital banking inverts every one of those assumptions.

When a neobank serves tens of millions of customers, every one of them interacts with the institution exclusively through a web or mobile-web interface. The interface is not a wrapper around a banking product, it is the banking product.

Page-load speed matters more here than almost anywhere else, because the conversion at stake is not an e-commerce purchase but whether a customer completes a fund transfer, finishes an account opening, or trusts the platform with their salary.

Digital banking customers reach their accounts from smartphones, tablets, laptops, and desktops, switching between Chrome on Android, Safari on iOS, Firefox on Linux, and Edge on Windows, sometimes within a single session.

A customer might initiate a transfer on their phone at lunch, review it on a work laptop, and confirm it on a tablet at home.

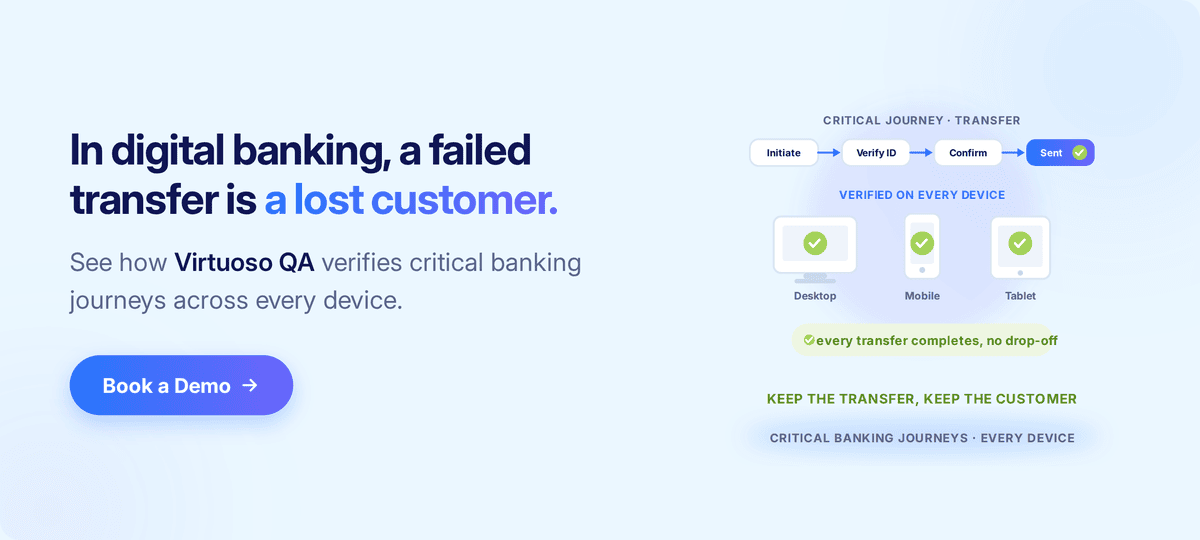

Each of those touchpoints has to deliver consistent rendering and functional reliability. A misaligned button on one browser, a dropdown that fails at a specific resolution, or a session that expires inconsistently across devices does not just create frustration. In banking it creates fear, and fear drives churn.

The composable banking movement has changed how banking software is built and deployed.

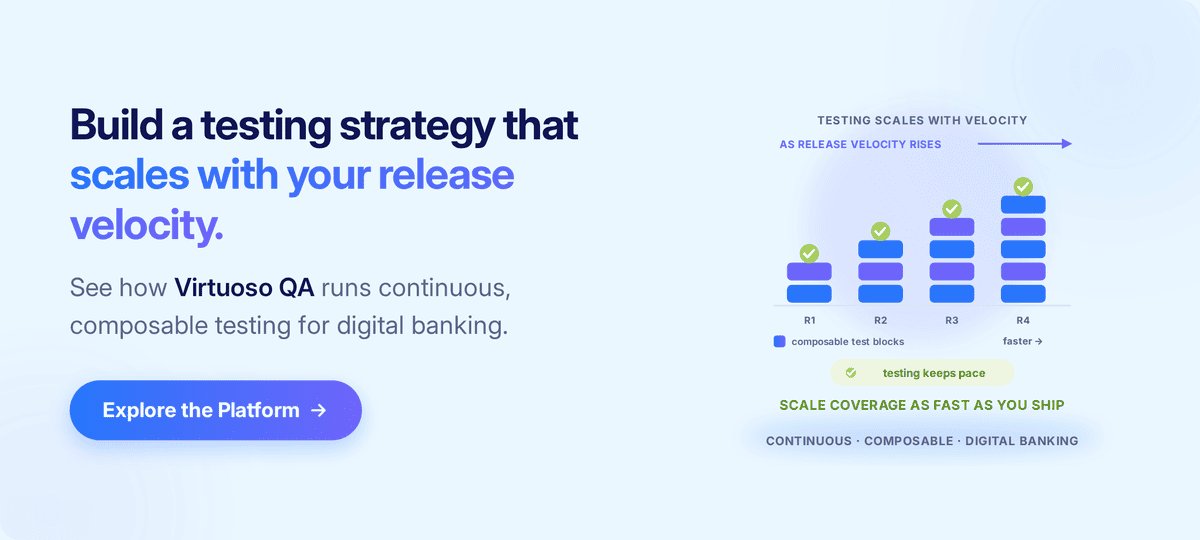

Every release is a potential regression. Every update to the core platform, every new API integration, every tweak to the onboarding funnel needs validating across the full matrix of supported devices and browsers.

Manual testing cannot keep pace, and traditional scripted automation breaks faster than it can be maintained.

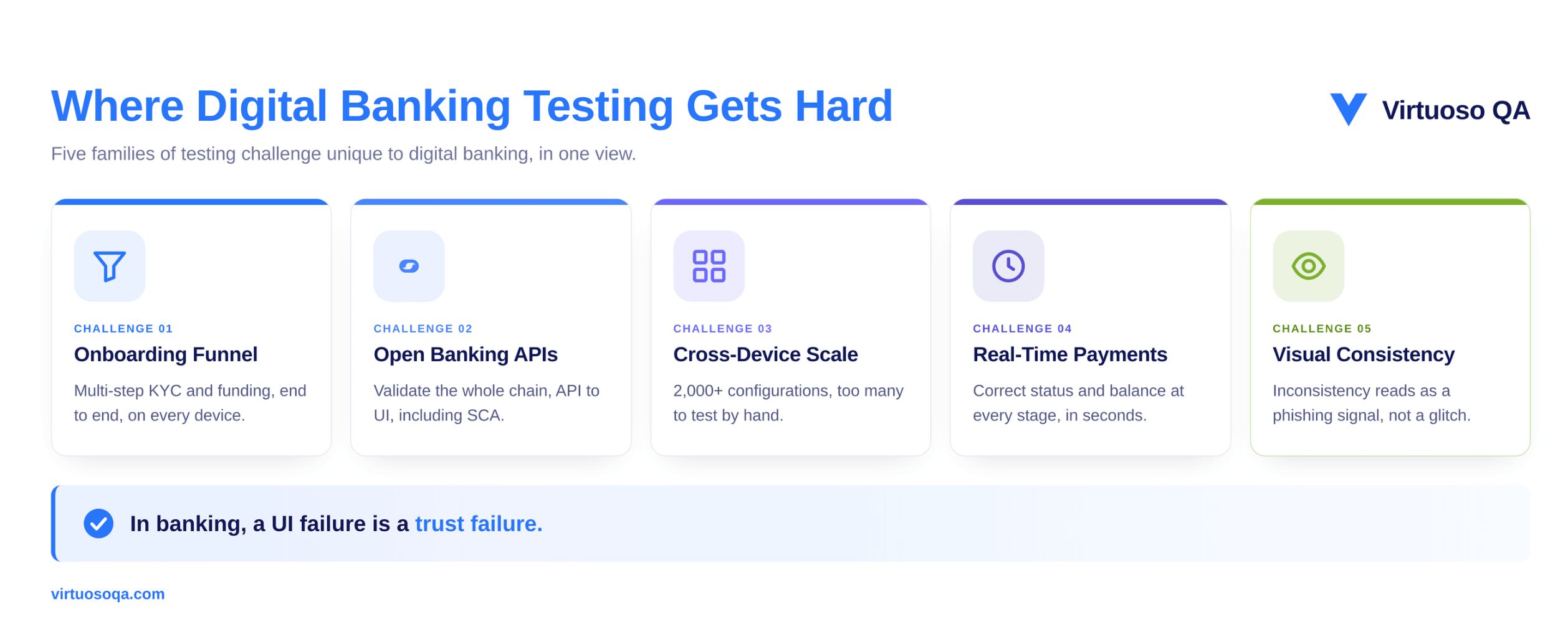

Five challenges account for most of the testing difficulty in modern digital banking, and naming them is the first step to building a strategy that holds.

Digital bank onboarding is the most complex user journey in consumer fintech, typically involving identity-document capture, facial verification, personal-data entry, address validation, terms acceptance, and initial funding, all of which must work flawlessly and in sequence across every supported device and browser.

A broken onboarding flow does not just lose a customer, it wastes the marketing cost of acquiring that customer, which for neobanks is substantial.

The funnel has to be tested end to end, from the first marketing landing page through to account activation, which means validating form submissions, file uploads, multi-step navigation, conditional logic, and third-party KYC integrations all working together.

Open banking regulation, driven by PSD2 in Europe and similar frameworks globally, requires banks to expose APIs that let third-party providers access account information and initiate payments, and PSD3 is already in development with stricter requirements around API standardisation, consent management, and fraud prevention.

This creates a challenge that is both technical and regulatory. The front-end experience has to display data retrieved from third-party aggregators correctly, payment-initiation flows must work consistently when triggered from external applications, and Strong Customer Authentication flows must function across devices without creating friction that causes abandonment.

The critical gap is that traditional approaches treat UI and API as separate concerns, whereas digital banking needs unified testing that validates the entire chain, the API call, the data transformation, the UI rendering, and the user interaction, within a single journey.

A major neobank typically supports Chrome, Safari, Firefox, Edge, Samsung Internet, and Opera across iOS, Android, Windows, and macOS. Once you multiply browsers by operating systems by screen resolutions by device types, the matrix easily exceeds 2,000 configurations.

Testing even the core flows of login, balance check, transfer, payment, and statement download across that matrix manually would consume thousands of hours per release cycle.

Most banks compromise by testing a subset and hoping the rest works, but in a sector where a single visual inconsistency can trigger a support call and a single functional failure can trigger a regulatory inquiry, hope is not a testing strategy.

Digital banking operates in real time, with customers expecting instant payment confirmation, immediate balance updates, and real-time notifications. Testing these flows means validating that front-end displays accurately reflect back-end state changes with minimal latency.

This is particularly demanding with faster-payment schemes such as UK Faster Payments, SEPA Instant, and FedNow, where the window between initiation and settlement is measured in seconds.

The testing must verify not just that the transaction completes, but that the customer sees the correct status at every stage, pending, processing, and completed, with accurate timestamps, correct amounts, and proper formatting for their locale and currency.

In banking, visual inconsistency erodes trust disproportionately. A button that renders differently across browsers, a font that substitutes unexpectedly, or a logo that shifts on certain screen sizes is not a cosmetic issue, because it makes customers question whether they are on a legitimate site. In an industry plagued by phishing and lookalike fraud, visual consistency is a security signal.

The traditional approach to testing banking applications, whether through Selenium scripts, Cypress frameworks, or recorded test tools, was designed for a different era, and it shares common failure modes that make it unsuitable for modern digital banking.

Modern banking interfaces are built with frameworks such as React, Angular, and Vue that generate dynamic element identifiers, so every time the front end is updated or redeployed, element IDs, class names, and DOM structures can change.

Locator-based automation that depends on those identifiers breaks immediately, creating a maintenance burden that grows with the size of the suite.

For a bank running a large automated suite at weekly cadence, even a small breakage rate per release means a steady stream of tests needing manual investigation and repair before a single new test is written.

Most traditional frameworks are designed for either UI testing or API testing, not both at once, yet digital banking flows constantly cross that boundary.

A customer initiates a payment through the UI, the front end calls an API, the API processes the transaction, a webhook triggers a notification, and the UI updates to reflect the new balance.

Testing this end to end needs a platform that can combine UI interactions with API validations within a single journey, verifying that what the customer sees reflects what the back end actually processed.

Running tests across more than 2,000 device and browser configurations requires cloud infrastructure that traditional frameworks were not built to leverage.

Setting up and maintaining a device grid, managing parallel execution, and aggregating results across configurations is an infrastructure problem that consumes engineering effort better spent building banking products.

The testing challenges in digital banking are not incremental tweaks to old problems, they represent a shift in what testing has to accomplish, and AI-native testing, built from the ground up with machine learning and natural language processing at its core, addresses them architecturally rather than through workarounds.

AI-native test platforms allow test creation in plain English that maps directly to banking processes. Instead of writing code to locate elements and simulate clicks, a QA or business analyst writes steps such as navigate to the transfers page, enter an amount, select the source account, and verify the confirmation shows the correct amount and recipient.

This has two advantages for banking teams. It makes tests readable by the compliance and audit stakeholders who need to confirm that testing covers regulatory requirements, and it accelerates test creation dramatically.

When a composable platform pushes an update that changes element identifiers or restructures a page, AI-native self-healing detects the change and updates test locators without human intervention, which removes the maintenance spiral that makes traditional automation unsustainable at banking velocities.

Mature self-healing reaches around 95 percent user acceptance, the level at which the majority of UI changes are absorbed automatically and the QA team is freed to expand coverage rather than repair broken tests.

Cloud-native execution across more than 2,000 operating-system, browser, and device configurations means a bank can validate every critical journey across the full customer matrix without maintaining any testing infrastructure, with tests running in parallel and delivering results in minutes rather than the hours or days sequential execution would take.

AI-native platforms like Virtuoso QA integrate API validations directly within UI journeys, so a single test can navigate the interface, initiate a payment through the UI, validate the API response, verify database state through SQL queries, and confirm the UI updates correctly, all in one executable journey.

For open banking, this means validating the entire PSD2 flow, third-party authorisation, consent capture, data retrieval, and front-end display, in a unified test that mirrors the real customer experience rather than testing fragments in isolation.

Automated visual comparison captures screenshots across every supported browser and device and flags pixel-level differences that could undermine trust.

For digital banks where the interface is the brand, this ensures every customer sees the same consistent experience regardless of how they access the platform.

A strategy that holds at neobank velocity comes down to a handful of deliberate choices.

Virtuoso QA is the trust layer for digital banking, built AI-native to keep customer-critical journeys working as releases ship weekly and the platform underneath keeps moving.

Try Virtuoso QA in Action

See how Virtuoso QA transforms plain English into fully executable tests within seconds.